We believe that the current implementation effect of the pilot area will improve the certainty of the comprehensive fall in 2017. This paper focuses on the analysis of the impact of the graded diagnosis and treatment on the industrial chain of the laboratory.

The amount of test + the quality of the test, the impact of the graded diagnosis and treatment on the laboratory. The direct impact of sub-diagnosis on the laboratory is the change of the inspection volume of different levels of hospitals. At the same time, the improvement of the requirements of the inspection of the basic level puts high demands on the inspection results. We look at both quantity and quality:

The test volume migrated to the grassroots level, and the tertiary hospital examined structural changes. After the first diagnosis of multiple diseases, the primary examination will be directly increased. When the diagnosis of medical treatment is changed, more patients will be diagnosed at the grassroots level regardless of the disease, and the first examination will be transferred from the third level to the first and second level hospitals; The number of first-time hospitals declined, the number of referrals increased, and the overall level remained at a stable level. At the same time, as the type of disease changed from ordinary to difficult, the demand for special inspection was significantly higher than that of general examination. The inspection category may be based on general inspection. The main change to the special inspection.

The demand for referrals will increase, and mutual recognition of regional inspections will become a development trend, and the level of inspection at the grassroots level will be increased. Due to the process of referrals, etc., the number of consultations has increased, and mutual recognition of regional test results is expected to be implemented in a wide range to reduce the number of repeated inspections and further reduce costs. Correspondingly, the products used by hospitals within the scope of mutual recognition are in quality. There are higher requirements.

In 2010, the Health Planning Commission issued a notice on promoting the mutual recognition of inspection results at the same level of medical institutions. At present, the first test results are mutually recognized and implemented in October 2016 in 131 medical institutions in the Beijing-Tianjin-Wing region (third-level hospitals + The medical examination center has implemented mutual recognition of 27 clinical test results. Although the mutual recognition of short-term and short-term results will only be implemented in medical institutions at the same level, we believe that the regional test results are mutually recognized based on the needs of grading medical treatment and avoiding repeated over-examination. The future is expected to expand to all levels of medical institutions in the region, including hospitals below the tertiary level and regional inspection centers.

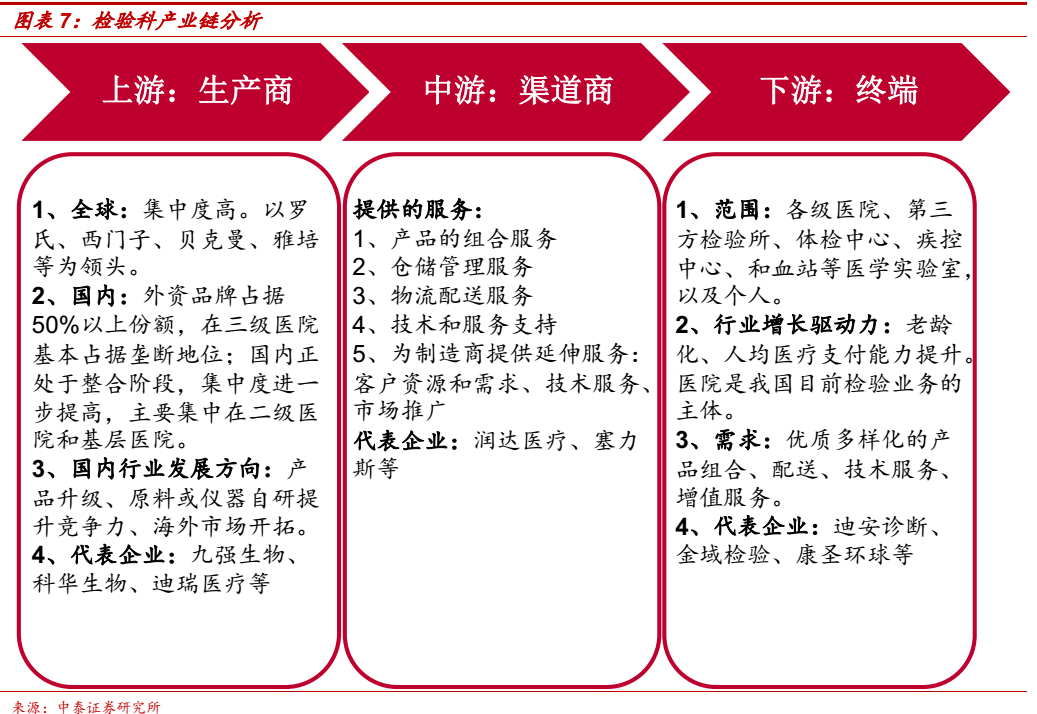

The grading diagnosis and treatment will bring about a major change in the competition pattern of the upstream and downstream aspects of the laboratory, as the end user of the diagnosis. We analyze its industrial chain:

1. The upstream is the manufacturer of diagnostic products, including the production of reagents and instruments;

2, the middle reaches is the product distribution channel, due to the wide variety of diagnostic products, most manufacturers more than 90% of the products are sold in the distribution model, agents are mainly responsible for hospitals and other channel development, product logistics and after-sales and other value-added services to improve customer stickiness, due to direct docking Terminal, so the circulation channel is very important in the diagnostic industry, and the bargaining power to the upstream is stronger;

3. The downstream is the user of the diagnostic products including the laboratory and the third-party medical examination. Currently, due to the rapid development of POCT products, some varieties will be directly applied to consumers (patients).

Distribution of industrial chain output: upstream 43 billion, midstream 95.6 billion, downstream 147.1 billion. According to the 2015 edition of the China Health and Family Planning Statistical Yearbook and the data of Saibai Blue, the total hospital revenue in 2014 was 1,661.173 billion yuan. We assume that the third-level hospitals account for 7.5% and the secondary hospitals for 10%. 12% of the first-level hospitals and an annual growth rate of 6% calculated that the terminal diagnostic market in 2015 was 147.1 billion yuan. The price of products entering the hospital was calculated at an average of 65%, and the market price of the middle reaches was 95.6 billion yuan. The ex-factory price of the products was based on the channel price. For the calculation of 50%, the upstream market is 43 billion yuan.

Mobile Suction Unit,Medical Suction Unit,Portable Suction Device,Portable Medical Suction

ZHEJIANG FOMOS MEDICAL TECHNOLOGY CO.,LTD. , https://www.ifomos.com